Steady Slaughter Reported For October But Still Down on 2012

UK - Cow slaughter increased last week to support meat supplies which were reported as steady, write Livestock and Meat Commission analysts. 28 October 2013

28 October 2013

2 minute read

2 minute read

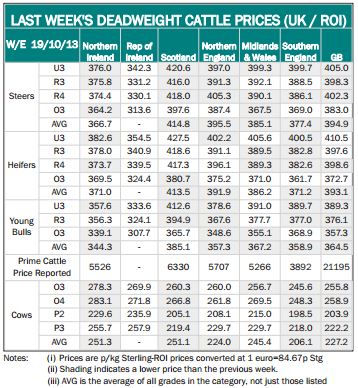

Deadweight Cattle Trade

Quotes from the plants for U-3 grade prime cattle remained steady this week, ranging from 364-368p/kg across the plants. The in spec bonus of 8-14p/kg continues to be available for steers and heifers.

Producers should consult individual processors as the criteria and level of bonus available for in spec cattle varies across the plants. Quotes for O+3 grade cows have come back to 270-280p/kg this week, write LMC experts. .

The plants have reported steady supplies of cattle with throughput of prime cattle last week totalling 7,087 head. This is 307 head less than the previous week and 200 head behind the corresponding week in 2012 when 7,287 head were slaughtered.

The cow kill in NI last week increased to 2,293 head, an increase of 274 head on the previous week. Imports from ROI last week for direct slaughter were similar to the previous week and consisted of 745 prime cattle and 204 cows, with a total of 244 cows exported from NI for slaughter in ROI plants. Meanwhile exports of cattle from NI to GB for direct slaughter increased on previous weeks to consist of 306 prime cattle and 62 cows.

Average steer and heifer prices in NI last week were within a penny of the previous week at 366.7p/kg and 371.0p/kg respectively with R3 steer and heifer prices showing a similar trend. Meanwhile in GB average steer prices were back by 2p/kg to 394.9p/kg with average prices across the GB regions showing a 2-3p/kg decline with the exception of Northern England where average prices were back by half a penny to 395.5p/kg.

Average heifer prices in GB were back by 1.5p/kg to 393.1p/kg. Average prices in Scotland and northern England were back by 1p/kg on the previous week while prices in the Midlands were unchanged at 386.2p/kg. Heifer prices in Southern England were back 5.8p/kg to 371.2p/kg.

Average cow prices in NI remain the strongest in the British Isles at present. Young bull prices in NI were back by half a penny to 344.3p/kg last week while prices were back in GB by 4.3p/kg to 364.5p/kg. The strongest declines were recorded in the Midlands and Southern England where prices were back by 5.6p/kg and 7.1p/kg respectively.

Tighter supplies of cattle in ROI have seen an improvement in the deadweight trade for all classes of cattle. The R3 steer and heifer prices increased by the equivalent of 5p/kg last week to 331.2p/kg and 340.9p/kg respectively. Deadweight prices in ROI remain behind NI levels with a price differential of 44.6p/kg for R3 steers and 37.1p/kg for R3 heifers.

The Weeks’ Marts

Finished first quality steers sold from 215-238p/kg (avg 222p/kg) this week while second quality sold from 160-214p/kg (avg 195p/kg). Finished heifers sold to an average of 217p/kg for first quality while second quality sold to an average of 195p/kg. Well fleshed beef cows sold from 140-193p/kg (avg 157p/kg) with second quality selling from 112-139p/kg (127p/kg).

A slightly quieter trade for forward store cattle saw first quality bullocks 400-500kg sell to an average of 219p/kg while first quality heifers over 450kg sold to an average of 208p/kg.

.JPG)

TheCattleSite News Desk