Dairy: World Markets And Trade

During the first half of 2010, international dairy markets were surprisingly strong with the price of Oceania butter and cheese averaging around $4,000 ton while skimmed milk powder (SMP) averaged above $3,000 ton. 16 August 2010

16 August 2010

10 minute read

10 minute read

This appears to have been due to a combination of tight dairy product supplies following lower than anticipated milk production in Oceania (primarily New Zealand) coupled with a modest recovery in global economic activity which stimulated demand. Although there are significant government held surplus volumes of SMP and to a lesser extent butter available in the EU-27, these quantities are being carefully metered out in order to minimize any negative impact on markets. To date, SMP intervention stocks for commercial use remain unsold while some 60,000 tons has been allocated for use in domestic aid programs. The EU has clearly signaled that it will not accept SMP bids that could undermine market prices and potentially impact dairy farmers. In the United States, the previously held US CCC held stockpile of SMP was largely channeled into domestic assistance programs during 2009 and early 2010.

There are signs, however, that global dairy prices are set to ease in the coming months. The recent Fonterra (Global Dairy Trade) auction held in early July, while arguably not reflecting a fully transparent market, indicated a month-to-month drop of 10-15 per cent for butter, SMP, and whole milk powder (WMP). In the EU, prices of SMP and whey have slipped while WMP, cheese, and butter remain at relatively stable at surprisingly high levels. Irrespective, any decline is unlikely to signal a dramatic pull-back in prices since the fundamental conditions governing supply and demand in international markets are unlikely to change radically for the balance of 2010. In the United States and the EU, domestic dairy markets have shown marked improvement from 2009 and forecasts do not point to a sharp drop in prices that would trigger government purchases of surplus products.

It is likely that the correction in prices is more a reflection of anticipated increase in supplies as the new Oceania season approaches rather than a downshift in demand. The current key economic indicators, particularly for the emerging markets in Asia, remain positive with annual world Gross Domestic Product (GDP) growth slated to reach 3.5 (3-4) per cent in 2010 – up from - 2.0 per cent in 2009. In Asia, GDP is expected to grow by nearly 8 per cent while the key market of China is forecast to expand by 9-10 per cent. Mexico – a major market for US dairy commodities – is also projected to recover with economic output pegged to expand by almost 4.5 per cent.

In the United States, demand for dairy products should remain fairly firm since GDP growth is forecast to grow by 3-4 per cent; a sharp turnaround from 2009 when the economy shrank by 2.4 per cent. Nevertheless, persistent unemployment at around 9-10 per cent remains a concern. In the EU (Eurozone), GDP is likely to grow by a modest 1 per cent; however, the sovereign debt issues particularly in Greece are wildcard factors that could roil markets.

From the supply perspective, while New Zealand’s new season milk production may regain it’s 3-4 per cent annual increase, the prospect of Australia reversing years of declining milk output is becoming a dimmer prospect as drought is becoming more the norm and rain the exception. Further, Oceania stocks for all the major dairy commodities particularly WMP are on the low side and any pick-up in demand or minor interruption in supply could rapidly translate into higher prices. In the United States and the EU, while milk supplies are expected to increase it appears that a further significant demand draw on internal supplies could pressure prices. In the United States, the recent jump in butter prices may well have been driven by the prospect of export sales. Cheese prices could follow a similar path.

Milk Production: 2010 Forecast Summary

| Summary of Major Milk Producer Forecasts for CY 2010 (1,000 Metric Tons) |

|||||

|---|---|---|---|---|---|

| 2008 | 2009 | 2010 (Dec. 2009 for.) | 2010 (July for.) | Change 10’ for. |

|

| Australia | 9,500 | 9,670 | 9,570 | 9,200 | - 4% |

| EU-27 | 133,848 | 133,700 | 134,000 | 134,000 | 0% |

| New Zealand | 15,141 | 16,601 | 17,021 | 16,726 | - 2% |

| United States | 86,174 | 85,874 | 85,230 | 86,710 | + 2% |

| Note: Australia July-June, New Zealand June-May year | |||||

Milk Production: 2010 Forecast Summary

The Australian milk production forecast was revised down as a result of low cow numbers and unexpectedly dry conditions that struck during the critical spring flush period. During the past five years Australian milk output has posted an annual growth rate (CAGR) of -2.4 per cent largely as a result of drought. For the future, milk production will likely remain constrained by low cow numbers which have dropped from 2 million in 2005 to an estimated 1.6 million in 2010. For the next season, should normal rainfall patterns materialise, even if the cow herd grew by 3 per cent and one assumed an optimistic milk per cow yield of 5.8 ton/hd), milk production would nevertheless still be below the levels attained in 2008/09.

New Zealand milk production was similarly affected but by a late-season drought on North Island which led to a downward adjustment in the forecast. For the year, milk output is now expected to expand by 1 per cent – well below the 3 per cent originally forecast. Nevertheless, farmers are expected to reap the reward of high global product prices this year and next as the milk payout at NZ$6.10/kg milk solids is the second highest recorded. Next season there is speculation that the payout will be higher. Consequently, assuming normal weather, milk output next season has the potential to expand by 2-3 per cent which could translate up to an additional 500,000 tons of milk. Over the longer term, South Island, which now accounts for slightly over a third of total New Zealand production, is likely to experience the most growth since it has the potential to convert substantial tracks of land for sheep and beef to dairy.

In the EU-27, milk production is anticipated to remain fairly steady although an improved milk yield per cow will lead to a marginal increase in total production. There has been some debate regarding the extension of quotas; however, at present, the proposal to end milk production quotas by 2015 stands.

In a reversal, annual US milk production in 2010 is expected to grow by 1 per cent largely as a result of higher milk yield per cow. Milk feed margins are anticipated to improve over 2009 due to a combination of lower feed costs and higher milk prices. For 2010, the annual all milk price is projected to average $15.80/cwt to $16.10/cwt which is a sharp improvement in comparison to the average of $12.84/cwt dairy farmers received in 2009. Lower feed costs and improved supplies of forage are expected to support improved milk per cow while increased profitability will mitigate the decline in cow numbers.

Cheese:

For 2009/10 (June-May), the New Zealand cheese production estimate is revised down from th previous forecast resulting in an annual 12 per cent drop in comparison to the previous year. Exports, however, are estimated to have grown marginally over the previous year which was likely sustained by a drawdown in stocks. It appears that strong returns from exports of WMP are channeling a significant portion of New Zealand’s manufacturing milk into the production of WMP.

The Australian cheese production estimate remains largely unchanged from the previous forecast and year-over-year output is expected to be slightly down. The export forecast has also been lowered but cheese shipments are still expected to have increased over the previous year by 18 per cent which are expected to be supplied by stocks.

The EU-27 cheese production forecast was raised by 1 per cent from the prior forecast and is expected to account for most of the additional manufacturing milk forecast for 2010. Returns driven by strong domestic and export demand are anticipated to favor the production of cheese for the balance of the year. The pace of exports has been exceptional in the first half of 2010 and the export forecast is raised by 85,000 tons (18 per cent) from the December 2009 forecast to 560,000 tons.

In the United States, prices for 2010 are forecast to favour the production of butter/powder at the expense of cheese and annual cheese production is expected to drop 1 per cent from the previous year. The cheese export forecast is raised by 18,000 tons from the December forecast to 140,000 tons which represents a nearly 30 per cent improvement over the previous year. In the period Jan-May 2010, Mexico has been the major destination accounting for nearly 30 per cent of the 64,000 tons exported.

Butter:

The New Zealand butter production estimate was raised slightly from the previous forecast but the year-on-year increase is a modest 2 per cent. Butter exports, however, have been fairly robust due to attractive global prices. Consequently, the export forecast was revised up 12 per cent which is expected have led to a drawdown in stocks. In Australia, butter production is estimated to have been scaled back relative to last year but as in New Zealand, the strength of the export market is expected to have led to a drop in stock levels.

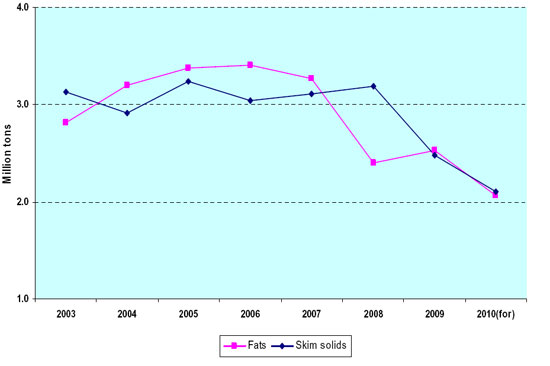

In the EU-27, 2010 butter output is expected to drop by 1.5 per cent over the previous year as milk is shifted into the production of cheese. Exports, however, are anticipated to increase by 15 per cent over 2009 largely supplied by releases from intervention stocks. At present, intervention stocks stand at 52,000 tons and a substantial amount – in the order of 51,000 tons – has been slated for release during the May- September period for use in domestic assistance programs. Despite this influx of butter, domestic prices are surprisingly strong and holding at $2.20/lb – some 27 per cent higher than at the same period last year. The US butter export forecast is raised by one third from the previous forecast but at 32,000 remains well below levels obtained in 2007 and 2008. There is some expectation that should the outflow of butter to the export market increase significantly; domestic prices will rise to effectively ration supplies. There appears to be some evidence of this effect already as the monthly CME price average has increased in consecutive months since February 2010 ($1.36/lb) through June 2010 ($1.64/lb). Price increases appear to also reflect lower available supplies of milk fat as the national milk fat test percentages for the first half of the year have been below last year’s comparable period. This may also explain to a certain extent why end-May cold storage stocks were down 16 per cent in comparison to the same period last year.

SMP:

Oceania exports for SMP are estimated to have grown by 11 per cent over last year largely due to a sharp upward revision (23 per cent) in the forecast for New Zealand. Since production is only expected to have expanded slightly, these shipments likely led to a reduction in stocks.

Due to the strong pace of shipments in early 2010 particularly to such destinations as Algeria, Russia, and Indonesia, the EU-27 export forecast is raised by 42 per cent from the previous forecast. Intervention stocks which stood at around 257,000 tons at the beginning of the year are currently at around 236,000 tons and are forecast to drop to 200,000 tons by the end of the year.

The US export forecast for SMP is raised by 3 per cent from the December forecast with total shipments in 2010 expected to grow by 20 per cent over 2009. Shipments during the first quarter at 54,000 tons were disappointing in light of the favourable price differential between the US and world market prices. Shipments in the first two months of the second quarter jumped to 67,000 tons and US SMP is expected to remain relatively competitive for the balance of the year.

Whole Milk Powder (WMP):

The New Zealand WMP production estimate is raised slightly to 760,000 tons which is a less than a 1 per cent increase over the previous year. Exports, however, totaled 894,000 tons which represents a 35 per cent increase in comparison to the 2008/09 year. This means that a substantial drawdown in WMP stocks likely occurred. China has been by far the biggest purchaser of New Zealand WMP, accounting for some 26 per cent of total exports. More impressively, China more than doubled its purchases from the previous year and a continuation of such purchases is likely to be a bullish factor for the balance of this year.

The EU-27 export forecast is revised down 10 per cent from December and WMP exports are expected to drop by 8 per cent to 425,000 tons in comparison to the previous year. It appears that relatively firm prices within the EU-27 may have reduced the competitiveness of WMP leading to a 10 per cent drop in early year (January-April) shipments of WMP.