US farmer sentiment declines in September while inflation worries rise

Perdue University's Ag Economy Barometer shows US lower farmer sentiment for September 2021, recording its weakest reading since July 2020. 19 October 2021

19 October 2021

5 minute read

5 minute read

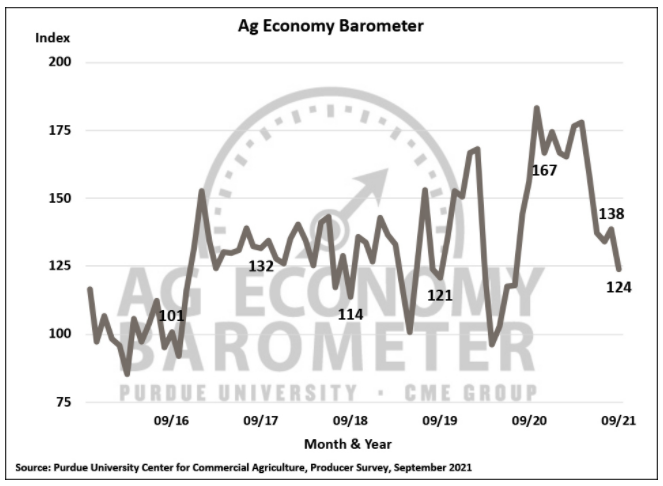

Sentiment among agricultural producers weakened in September as the Ag Economy Barometer declined 14 points to a reading of 124. This is the weakest farmer sentiment reading since July 2020 when the index stood at 118.

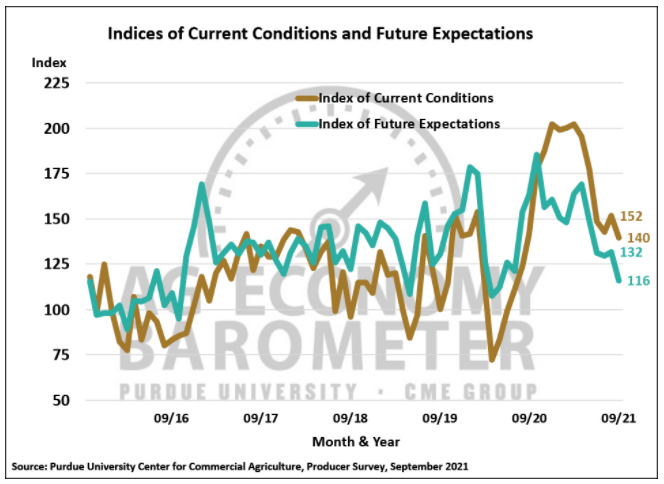

Producers were less optimistic about both current and future conditions on their farms and the agricultural sector than they were a month earlier. The Index of Current Conditions declined 12 points to 140 this month, while the Index of Future Expectations fell 16 points to 116.

This month’s Future Expectations Index reading was its lowest since May of 2020 when the nation was still in the throes of the pandemic’s first stage. The Purdue University-CME Group Ag Economy Barometer sentiment index is calculated each month from 400 US agricultural producers’ responses to a telephone survey. This month’s survey was conducted from 27 to 29 September 2021.

Figure 1. Purdue/CME Group Ag Economy Barometer, October 2015-September 2021.

Figure 2. Indices of Current Conditions and Future Expectations, October 2015-September 2021.

The Farm Financial Performance Index, with a reading of 110, was unchanged from a month earlier, but there was a shift among producers in their responses used to compute the index. Fewer producers said they expected their farms’ financial performance to be about the same as last year, while the percentage of producers expecting both worse and better performance rose.

The percentage of farms expecting better performance, 36%, was four points higher than last month and the highest since May. The percentage of farms expecting worse financial performance also rose 4 points to 26%, in line with expectations earlier this summer, but substantially higher than in May when just 16% of farms said they expected worse performance this year than last. The difference in expectations among farms could reflect differences in how individual farms managed risk in a period of rapidly fluctuating commodity prices.

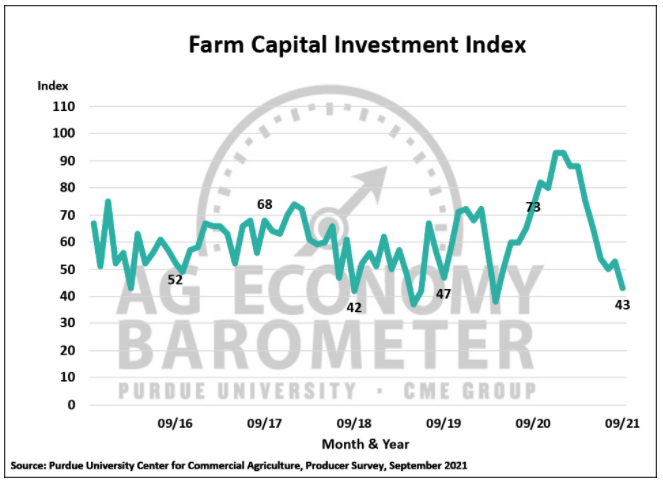

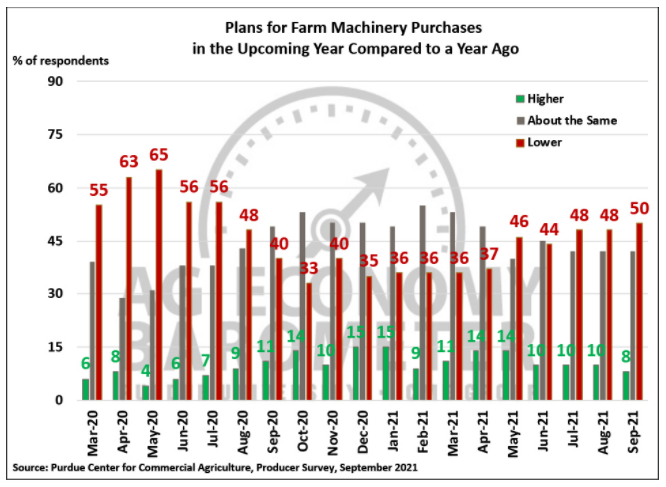

The decline in farmer sentiment was reflected in a weaker Farm Capital Investment Index. The index declined 10 points to a reading of 43, which was the lowest value for the investment index since April 2020. Moreover, the investment index is now down more than 50% since the beginning of the year. Farmers’ plans for machinery purchases were somewhat weaker than in August with just 8% of respondents planning to increase purchases in the upcoming year, down from 10% last month.

This month’s survey included a new question to capture the impact of supply chain challenges in the farm machinery industry on investment plans. Nearly half (45%) of respondents said that their farm machinery purchase plans have been impacted by low farm machinery inventories, which helps explain weak sentiment regarding whether or not now is a good time to make large investments in their farm operation.

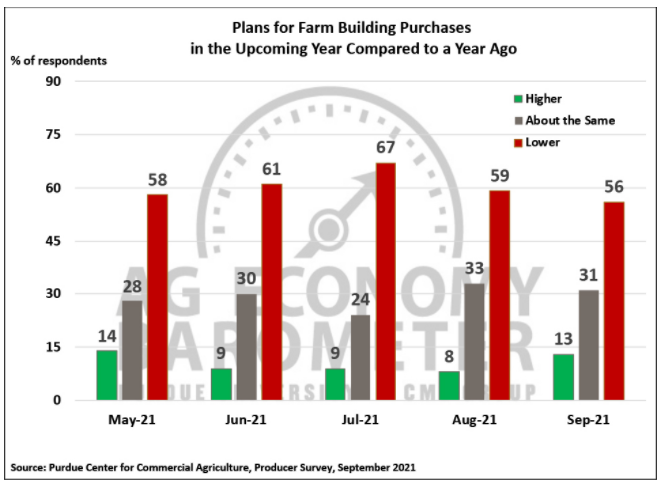

One bright spot was an improvement in farmers’ plans for new construction. New construction plans rose this month with 13% of respondents expecting to increase construction of grain bins and farm buildings compared to 8% expecting those purchases to rise on the August survey.

Figure 3. Farm Capital Investment Index, October 2015-September 2021.

Figure 4. Plans for Farm Machinery Purchase in the Upcoming Year Compared to a Year Ago, March 2020-September 2021.

Figure 5. Plans for Constructing New Farm Buildings and Grain Bins, May-September 2021.

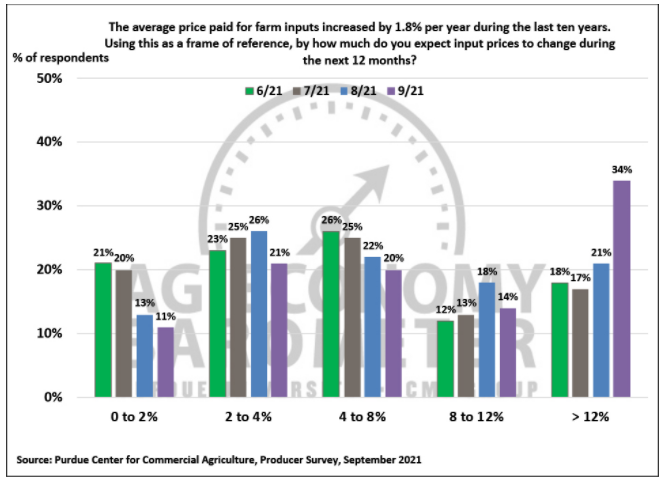

Concerns about rising input costs rose sharply in September, contributing to the weakness in farmer sentiment. This month, just over one-third of respondents said they expect farm input prices to rise by more than 12% in the upcoming year, which is more than 6 times the average farm input inflation rate of the last decade.

Moreover, inflation expectations were higher this month across the board. The percentage of respondents expecting input inflation to rise above 12% jumped from 21% last month to 34% this month, while responses to all of the lower inflation categories provided on the survey declined. Notably, the percentage of producers expecting input inflation to rise above 12% has doubled since July.

Figure 6. Farm Input Price Expectations During the Next 12 Months, June-September 2021.

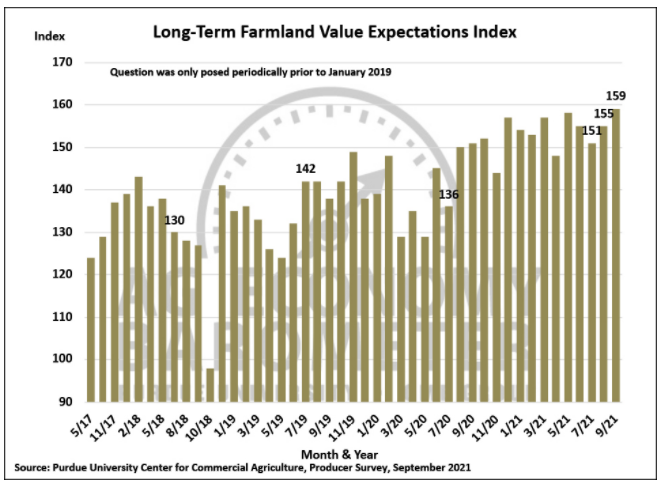

Despite weaker readings for both the Current Conditions and Future Expectations Indices, farmers remain bullish about farmland values. Both the short- and long-term Farmland Values Expectations Indices rose this month. The Long-Term Farmland Value Expectations Index hit a record high reading of 159, 4 points higher than a month earlier, while the short-term index rose 9 points to 155, which is the third-highest reading since data collection began in 2015.

Approximately half of the corn-soybean growers in our survey continue to say they expect farmland cash rental rates to rise in 2022 vs. 2021. Three out of ten respondents expect rates to rise by 10% or more, while 44% of respondents expect the rental rate increase to range from 5% to 10%.

Figure 7. Long-Term Farmland Value Expectations Index, May 2017-September 2021

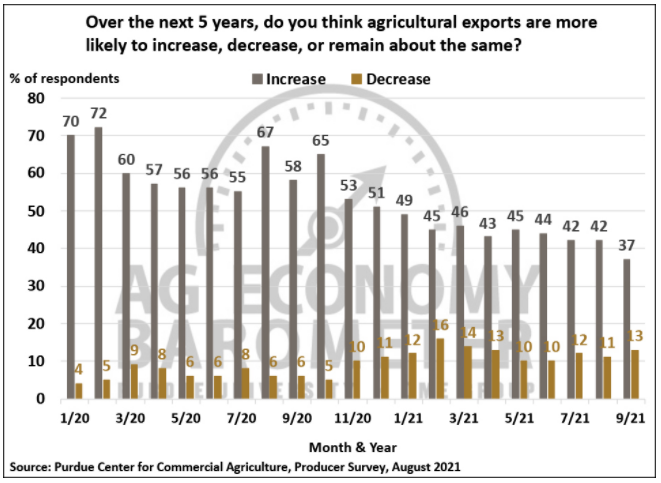

Farmer expectations regarding future agricultural trade prospects continue to weaken. In early 2020, seven out of ten producers said they expected agricultural exports to increase over the next five years. Since then, the percentage of farmers expecting agricultural exports to rise has been falling month-by-month, with just a couple of notable exceptions.

This month’s survey recorded the lowest percentage (37%) of producers expecting agricultural exports to increase since we first posed the question in early 2020. Concerns about the future of agricultural trade could be one of the reasons behind weakness in the Future Expectations Index.

Figure 8. Agricultural Export Expectations Over the Next 5 Years, January 2020-September 2021.

Wrapping up

Farmer sentiment weakened in September as agricultural producers reported both weaker current conditions on their farms and weaker expectations for the future. Although the Farm Financial Performance Index was unchanged this month, there was a shift in financial expectations with fewer producers expecting performance similar to last year and more producers expecting both better and worse performance than a year earlier.

Weaker farmer sentiment spilled over into the Farm Capital Investment Index, although over half of this month’s respondents said that low farm machinery inventories impacted their purchase plans. There was a sharp rise in farmers’ expectations regarding farm input price inflation with more than one-third of respondents expecting input prices to rise by more than 12% in the upcoming year.

Farmer optimism about future growth in agricultural exports continues to wane, and that, combined with concerns about a squeeze on operating margins, could be contributing to weakness in farmer sentiment. Despite the weakness in farmer sentiment, farmers remain bullish about farmland values with the Long-Term Farmland Values Index reaching a record high this month.